Denmark

Downloads

Further contacts:

Germany

- Federal Institute for Drugs and Medical Devices – EN Medical devices/DE Medizinprodukte

- Get on overview of the Catalog of assistive devices (DE)

- Apply to have your medical devices included in the catalog of assistive devices (DE)

Downloads

Webinars

Background information on the healthcare systems in brief

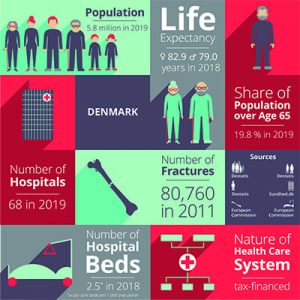

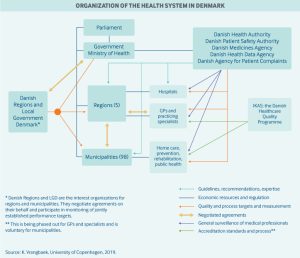

Healthcare in Denmark is provided by the local governments of the five regions, with coordination and regulation by central government, while nursing homes, home care, and school health services are the responsibility of the 98 municipalities.

Healthcare in Denmark is provided by the local governments of the five regions, with coordination and regulation by central government, while nursing homes, home care, and school health services are the responsibility of the 98 municipalities.

Danish government healthcare expenditures amount to approximately 10.4% of the GDP, of which around 84% is funded from regional and municipal taxation redistributed by the central government. Because basic healthcare is taxpayer-funded, personal expenses are minimal and usually associated with co-payments for certain services. Those expenses are for the most part covered by private health insurance.

Use of electronic health records is universal, and efforts are underway to integrate these at the regional level. For every 1,000 people in Denmark, there are about 3.4 doctors and 2.5 hospital beds. Spending on hospital facilities, at 43% of total healthcare spending, is above the average for OECD countries, even though the number of beds has decreased considerably in the last decade.

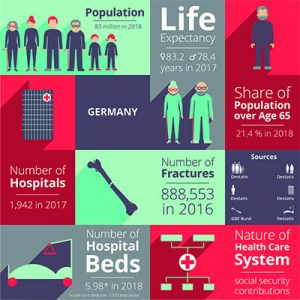

In Germany, the principle of self-administration applies: Although the Federal state sets the legal framework and tasks, the insured and contributors as well as the service providers organise themselves in associations that are responsible for providing medical care to the population.

The Federal state holds most university hospitals, while municipalities play a role in public health activities and hold about half of all hospital beds. Patients health insurance covers costs that are directly associated with the treatment in the hospital. The State in which the hospital is located finances so-called ‘investment costs’ such as diagnostic machinery, ambulance vehicles, and building maintenance. Source: “Report: Comparison of the Danish and German healthcare system“

The German health care system is supported and self-managed by many institutions and actors. The core area, also known as the first healthcare market, comprises the area of “classic” health care, which is largely financed by statutory health insurance (SHI) and private health insurance (PHI) including nursing care insurance. All privately financed products and services related to health are referred to as the second healthcare market. Source: “Bundesgesundheitsministerium – Gesundheitswirtschaft im Überblick“